Gold IRA Rules – What To Be Aware Of

The rules and regulations surrounding gold IRAs are really not that complicated, but in order to set one up correctly, everything needs to be handled with care to be completed in accordance with rules set forth by the Internal Revenue Service (IRS).

The reason why people think investing in physical bullion is an involved process is mostly due to the IRS, which is why it is imperative to work with a company that has it’s main focus on handling these type of accounts (see our recommended company here).

Most investors are accustomed to dealing with assets such as stocks, bonds, CD’s, ETF’s and mutual funds; not precious metals. However, as you’ll see the process is fairly straight forward and any experienced gold IRA company that works closely with an approved custodian should be able to help you walk through the steps easily.

So what are all the gold IRA rules you need to keep in the back of your mind…

Please also see our article: Gold IRA Rules & Regulations – FAQs

List of Gold IRA Rules

You need to be aware of these basic rules of a gold IRA, necessary for the best security and least risk:

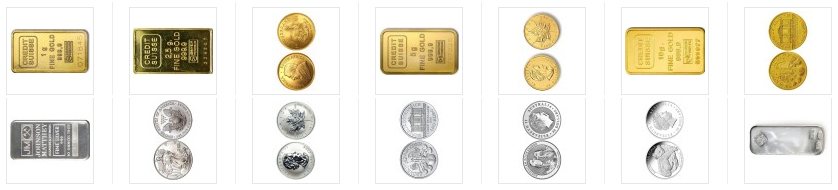

- No numismatic coins are allowed.

- IRS approved bullion only (see image below).

- You can open a self-directed gold IRA account directly with a new custodian.

- You can rollover or transfer funds from a previous retirement account (including 401(k), SEP, 403b, TSP) into a new self-directed gold IRA account.

- A gold IRA transfer is something you can do at any time if you have an existing account, however assets must go from custodian to custodian.

- A gold IRA rollover is when you receive your distribution from your current custodian directly, then deposit the funds into another custodian account within 60 days. If not you’ll be liable for taxes and penalties on the amount withdrawn.

- To keep your tax deferred status on this new gold IRA account, you can only rollover funds once a year.

While this may be a simple process, there are a couple of items that are worth repeating.

First, only bullion bars or coins can be bought for any IRA backed fund.

Secondly, the bullion bars and coins you are purchasing today are not going to be made available to you until you retire. Should you gain possession of these coins before they are placed in an IRS approved vault, then it is possible that they would not qualify to be placed into your IRA.

Numismatic coins are of a dubious value and are not recognized by the IRS to be a stable enough investment to qualify. Any company that tells you otherwise should be avoided at all costs, and yes we hear stories of companies steering investors towards these collectibles. It does happen from time to time, so be aware.

Gold IRA Tax Rules

Understanding the tax implications of a gold IRA is crucial for making informed investment decisions. Here’s what you need to know:

- Tax-Deferred Growth:

Like traditional IRAs, gold IRAs offer tax-deferred growth. This means you won’t pay taxes on the gains your gold investments make until you start taking distributions. - Contributions:

- Traditional Gold IRA: Contributions may be tax-deductible, depending on your income and whether you’re covered by an employer-sponsored retirement plan.

- Roth Gold IRA: Contributions are made with after-tax dollars, but qualified distributions in retirement are tax-free.

- Required Minimum Distributions (RMDs):

Traditional gold IRAs are subject to RMDs starting at age 72. You’ll need to take distributions and pay taxes on them, just like with a regular traditional IRA. - Early Withdrawal Penalties:

If you withdraw from your gold IRA before age 59½, you may face a 10% early withdrawal penalty in addition to regular income taxes. - In-Kind Distributions:

You can take distributions from your gold IRA in the form of physical gold, but the value of the gold will be treated as taxable income in the year you receive it. - Collectibles Tax Rate:

If you hold the gold outside of an IRA, any gains when you sell may be taxed at the collectibles rate (maximum 28%) rather than the lower long-term capital gains rate. - Roth Conversion:

You can convert a traditional gold IRA to a Roth gold IRA, but you’ll need to pay taxes on the converted amount in the year of conversion.

Remember, while gold IRAs offer unique benefits, they also come with specific tax rules and potential pitfalls. It’s always wise to consult with a tax professional or financial advisor to understand how these rules apply to your individual situation.

Contribution Rules for Gold IRAs

- For 2024, the annual contribution limit for IRAs (including gold IRAs) is $7,000 if you’re under 50 years old.

- If you’re 50 or older, you can make an additional “catch-up” contribution of $1,000, bringing your total limit to $8,000.

- These limits apply to the total contributions across all your IRAs (traditional and Roth), not just your gold IRA.

- Remember, you can only contribute earned income to an IRA.

Distribution Rules for Gold IRAs

Required Minimum Distributions (RMDs):

- Traditional gold IRAs must start taking RMDs when you reach age 73 (as of 2024).

- The RMD age will increase to 75 in 2033.

- Roth gold IRAs do not require RMDs during the owner’s lifetime.

Distribution Options:

- You can take distributions from your gold IRA in cash (after the custodian sells the gold) or as physical gold.

- If you take physical gold, its fair market value on the distribution date is considered income for tax purposes.

Gold IRA Rollover and Transfer Rules

You can roll over funds from a traditional IRA or 401(k) into a gold IRA without tax penalties, as long as you follow IRS rules.

The rollover must be completed within 60 days to avoid taxes and penalties.

You’re limited to one IRA-to-IRA rollover per 12-month period.

Prohibited Transactions:

- You can’t use your gold IRA assets as security for a loan.

- You’re not allowed to buy gold from or sell gold to your IRA.

- Violating these rules could result in your entire IRA being treated as a distribution, subject to taxes and penalties.

Gold IRA Withdrawal Rules

- Early Withdrawals: Taking money out of your gold IRA before age 59½ typically results in a 10% early withdrawal penalty, in addition to any taxes owed.

- Exceptions exist for certain situations like first-time home purchases, higher education expenses, or significant medical costs.

Home Storage Gold IRA Rules

According to the IRS, you cannot take physical possession of gold that is meant for you IRA. Therefore, you cannot store your IRA gold at your own home. If you’ve been hearing advertisements about storing your physical gold from an IRA at home, be wary. This is not advisable and could actually be illegal.

The IRS has issued a stern warning against this practice because the law states that one must store precious metals with a self-directed IRA third-party custodian. Don’t believe the hype about starting a LLC company and having the LLC name yourself as the trustee.

There is a long drawn-out process that also requires your application be approved by the IRS. Because the IRS has long caught on to this, the chances of approval are slim to none. You could even face fines, penalties, and extra taxes. Besides, creating an LLC is definitely not suitable for regular retirees.

Creating an LLC as trustee of your Gold IRA

Not recommended, but in any case, here are some of the home storage precious metals IRA requirements:

- You must have or create a limited liability company, in your name, and with a specially written operating agreement.

- After incorporation and audits, you must have a minimum net worth of at least $250,000.

- All employees and trustees of the company must put up a $250,000 fidelity bond as corporate insurance.

- Ownership of the trustee corporation must be divided between several people.

- Applicant must have verifiable fiduciary experience with a “reputable financial background” and prove to have had experience handling retirement funds.

- The trustee corporation for your IRA must have a business location that is open to the public.

- Applicant must have corporate legal counsel on retainer and provide a detailed audit by a qualified public accountant annually.

The bottom line is, since the IRS has never approved home storage gold IRAs, do it the right way. Have your Gold IRA administered by a custodian, also called a trustee (our top recommended trustee is below). So remember this when approaching precious metals companies… ‘IRA gold must be physically maintained in a depository by the custodian or trustee, not by the IRA owner.’

Self Directed Gold IRA Rules

Other self directed gold IRA rules you need to be aware of and should incorporate:

- Fully-insured and segregated precious metal storage (w/ a registered custodian)

- Hold metals on the books of a company or title only you control

- Avoid metals that can be hypothecated by the trustee, meaning lent out to cover anyone’s debts but your own.

- Assuring direct ownership, ensuring accounts are titled in your name or in the name of an entity you control

- Make sure promissory notes and certificates are third-party insured

- Avoid accounts that require the trustee to purchase metals at market price when requesting delivery

Interested in getting started toward setting up your gold IRA today?

We recommend first getting a copy of this free gold IRA Investor Kit which will answer all your remaining questions.

After you have read the material you can get in touch with this company to setup a gold backed IRA. They have the experience and know-how to help you establish your account with an IRS approved custodian.

We are currently recommending them as our highest rated specialized gold IRA company. To see why, take a look at this review.

The Bottom Line

Investing in precious metals through your retirement account can be an interesting way to diversify your savings. However, the rules can be tricky. Here are the key takeaways:

- You can invest in certain IRS-approved precious metals and coins.

- Never keep these investments at home or in your personal possession.

- Use approved trustees or depositories to store your precious metals.

- Understand the tax implications, including potential benefits and pitfalls.

- When in doubt, consult with a tax professional or financial advisor.

Remember, the goal is to make your golden years truly golden – not to create a treasure chest in your basement or an unexpected tax bill!